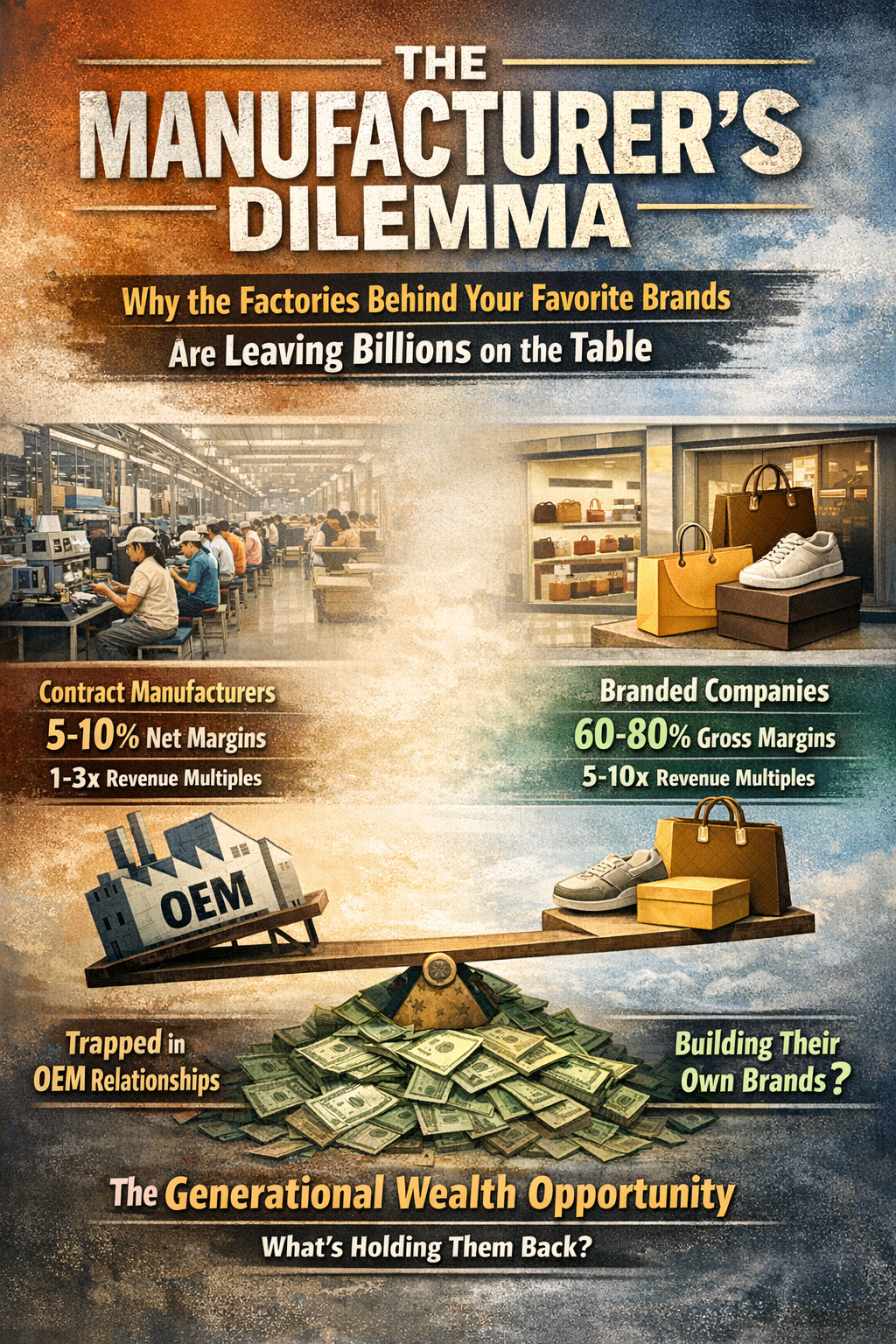

THE MANUFACTURER'S DILEMMA

“The Generational Opportunity For Manufacturers - Watch the Complete Video Below to Know More”

“Grab The Strategic Opportunity Today ——-Fill the form below & we’ll reach out to discuss more”

ABOUT THE AUTHOR

Pallavi Sehgal is the founder of PallaviSehgal.com & Punjab Capital, where she advises manufacturers and emerging brands on strategy, capital markets positioning, and brand building. With 15 years of experience at the intersection of luxury brand strategy and capital deployment, she works with founders navigating the manufacturer-to-brand transition.

Contact: ps@pallavisehgal.com | pallavisehgal.com

Why the Factories Behind Your Favorite Brands Are Leaving Billions on the Table

The economics are stark: contract manufacturers operate on 5-10% net margins while the brands they produce for enjoy 60-80% gross margins. At exit, manufacturers trade at 1-3x revenue; branded companies command 5-10x. Yet thousands of capable manufacturers across Asia remain trapped in OEM relationships, missing the generational wealth creation opportunity of building their own brands. This paper examines why—and what's changing.

THE GREAT VALUE GAP

Somewhere in Guangzhou, a factory is producing 10,000 skincare products per day. The formulation is world-class—organic, clean-label, effective. The facility is GMPC-certified, ISO 22716 compliant, and exports to 30 countries. The founder has 25 years of formulation expertise.

That factory earns $2 per unit. The brand selling those products earns $40.

This is the manufacturer's dilemma: possessing extraordinary capability while capturing a fraction of the value created. And it's not a marginal gap—it's a chasm.

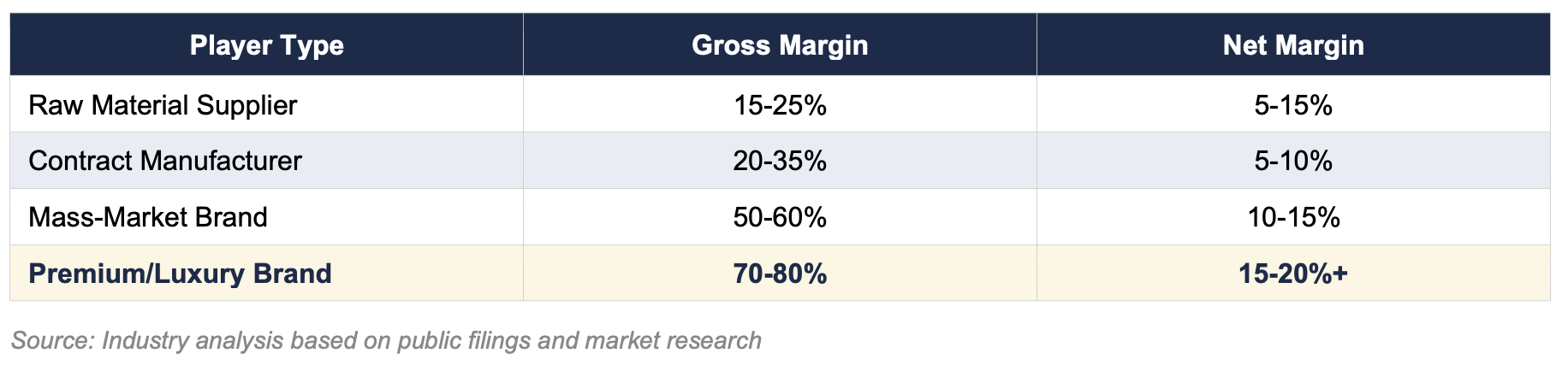

The Margin Reality

The beauty industry illustrates this starkly. Contract manufacturers typically operate on 5-10% net margins, competing on price and efficiency in a crowded market. Brand owners—especially in luxury and premium categories—enjoy gross margins of 60-80%.

The Valuation Multiplier

The gap becomes even more dramatic at exit. Manufacturing businesses typically trade at 1-3x revenue due to their capital intensity, thin margins, and limited differentiation. Consumer brands—particularly those with strong D2C channels and loyal customer bases—command 5-10x revenue multiples.

Consider two hypothetical businesses, each generating $10M in annual revenue:

Same revenue. 3x the enterprise value. This isn't theoretical—it's the arithmetic driving billions in wealth creation for founders who make the transition.

WHY MANUFACTURERS STAY STUCK

If the economics are so compelling, why don't more manufacturers make the leap? In my work with manufacturers across India, Southeast Asia, and China, I've identified five structural barriers that keep capable operators trapped in OEM relationships:

1. Competency Gap

Manufacturing and brand-building require fundamentally different capabilities. A factory owner may have mastered formulation chemistry, production efficiency, and quality control—yet know nothing about consumer psychology, digital marketing, or premium pricing strategy. The skills that made them successful in B2B manufacturing are largely irrelevant in B2C brand building.

2. Channel Blindness

Traditional manufacturers sell to purchasing managers at brand companies. They've never had to acquire a consumer, build a social media following, or manage a D2C website. The entire go-to-market architecture is foreign territory.

3. Capital Misallocation Fear

Manufacturing is capital-intensive. Factory owners are accustomed to investing in equipment, facilities, and inventory—tangible assets with predictable returns. Brand-building requires spending on marketing, content, and customer acquisition—intangible investments that feel like burning cash.

4. Relationship Risk

Many manufacturers fear that launching their own brand will cannibalize or jeopardize their existing OEM relationships. Major brand clients may see them as competitors rather than partners.

5. Generational Transition Inertia

In family-owned manufacturing businesses—common across Asia—the founder built wealth through operational excellence and risk management. Brand-building feels speculative and unfamiliar. Often, it takes a second-generation leader with different instincts to see the opportunity.

"The factories that make the world's best products are often invisible—and dramatically undervalued."

THE STRATEGIC OPPORTUNITY: WHY NOW

Several macro forces are converging to make manufacturer-to-brand transitions more viable than ever:

D2C Infrastructure is Mature

The tools required to reach consumers directly—e-commerce platforms, social media marketing, influencer partnerships, fulfillment networks—have become democratized. A manufacturer in Jaipur or Guangzhou can now access global consumers with the same infrastructure available to established brands.

Consumer Trust is Shifting

Brand loyalty has weakened. Younger consumers care more about product quality, values alignment, and social proof than legacy brand names. This creates openings for new entrants who can demonstrate genuine capability and authenticity—exactly what manufacturers possess.

The Asia Premium is Real

Western consumers increasingly recognize Asian manufacturing excellence. Japanese beauty, Korean skincare, and Indian Ayurvedic products command premiums precisely because of their provenance. Manufacturers can leverage this credibility rather than hiding their origins.

Private Equity is Hungry

Consumer-focused PE and VC funds are actively seeking founder-led brands with authentic stories and differentiated products. A manufacturer launching their own brand isn't just capturing margin—they're creating an asset class that attracts capital.

THE PATH FORWARD: A FRAMEWORK FOR TRANSITION

For manufacturers considering the transition, I recommend a phased approach that manages risk while building capability:

Phase 1: Foundation (Months 1-6)

• Audit existing capabilities—formulation expertise, certifications, production capacity

• Identify category opportunity—where does your capability meet underserved consumer demand?

• Develop brand positioning—premium, accessible luxury, heritage, innovation-led?

• Structure the venture—separate entity, board governance, capital allocation

Phase 2: Launch Preparation (Months 4-9)

• Product development—hero SKUs, packaging, pricing architecture

• Channel strategy—D2C website, marketplace presence, social commerce

• Marketing foundation—content strategy, influencer relationships, PR narrative

• Operational infrastructure—fulfillment, customer service, returns management

Phase 3: Market Entry (Months 7-12)

• Soft launch—controlled release to test positioning and operations

• Performance marketing—paid acquisition to establish baseline economics

• Community building—turn early customers into advocates

• Iterate and optimize—use data to refine product, messaging, and channels

Phase 4: Scale and Capital (Year 2+)

• Category expansion—adjacent products leveraging core capability

• Geographic expansion—additional markets with product-market fit

• Capital raise—growth equity to accelerate scaling

• Exit preparation—audit, governance, positioning for strategic or financial buyer

CONCLUSION: THE GENERATIONAL OPPORTUNITY

The global manufacturing landscape is at an inflection point. Decades of capability-building in Asia have created thousands of factories with world-class expertise—in formulation, materials science, precision engineering, and quality control. These capabilities were built serving global brands. Now, they can serve global consumers directly.

The barriers to brand-building have never been lower. The margin opportunity has never been clearer. The capital markets have never been more receptive to founder-led consumer brands with authentic differentiation.

For manufacturers willing to make the leap, the prize is extraordinary: transforming from a cost-center supplier into a brand that captures the full value of their capabilities. The arithmetic is compelling. The proof points exist. The infrastructure is ready.

The only question is who will move first.